“This is an outstanding accomplishment. It indicates the collective resolve of the people of India to embrace new technologies and make the economy cleaner.”

– PM Modi

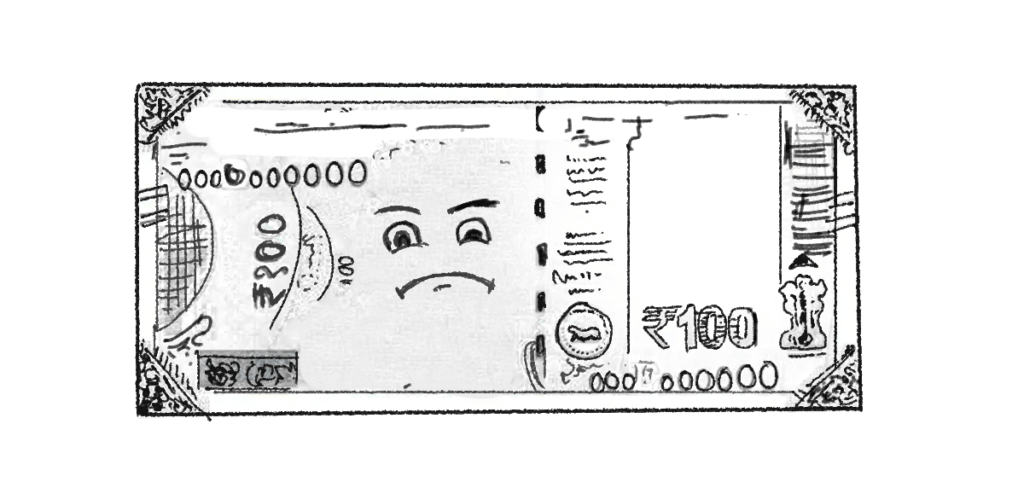

That’s PM Modi lauding UPI crossing 6 billion transactions in July. Like any icon, UPI has gained its share of admiration and envy. Last month, we intercepted a letter from a Rs. 100 currency note to UPI. It gets ugly. Reader discretion is advised.

Dear UPI,

I know everyone loves you. But I loathe you.

In my glory days, I used to be the only way to pay. People came from far and wide to ‘withdraw’ me from the bank. Safely tucked away in their wallets, I’d go everywhere with them. When we parted, I’d find home in a new wallet. Now ‘wallets’ are on the phone. They’re called e-wallets, I hear. Sheesh. And you, insufferable UPI, have found a way to pay through these e-wallets too.

I have, admittedly, been found in a few compromising positions – stuffed in a few pillowcases and under a few mattresses. But I’ve also found myself in pockets of migrant workers. 46 crore bank accounts were opened under the Jan Dhan Yojana. 18% of these accounts remain inactive. Which means that I’m still the lifeline for many Indians.

I’m also, admittedly, not cheap. The RBI and banks spend Rs.21,000 crores annually on currency operations. A Rs.100 note like me costs Rs.15-17 over a 4-year lifecycle in printing, distribution and storage. But let’s not pretend you’re ‘free’. Consumers and merchants don’t pay for you, UPI, only because payment service providers foot the bill. And it’s a hefty bill – Rs. 5500 crores annually. Even the Rs.1300 crore government subsidy comes from the taxpayers’ kitty.

Oh, and need I remind you of the war against my people – demonetization? Where my brethren, the beloved 500, was mercilessly hunted. I saw you sweep in and make hay while my tribe was under attack. Many wrote my obituary then as the cash to GDP ratio dropped from 12% to 8%. But I survived. And now I’m stronger than ever, with the cash to GDP ratio at 14.5%. My tribe is resilient. We found our way back into the hearts, pockets, and mattresses of our countrymen.

So, UPI – you insufferable teacher’s pet – don’t forget that while you may be the golden prince, I’m still the king.

Luke-warm (mostly cold) regards,

Mr. 100

After that salty take from Mr.100, let’s dive into this month’s FinTales menu.

Appetizers: snackable updates about recent fintech developments

Main-course: meaty stories about SEBI’s attempt to regulate online bond trading platforms and IRDAI’s push for datafication of motor insurance

Dessert: sweet news about UPI crossing 6 billion transactions and the road ahead

Take-away: interesting reads till the next FinTales meal

************************************************************************************************

Appetisers ?

?⚖️ Time for digital lenders to bite the bullet

RBI’s much-awaited digital lending guidelines are finally out. Here are the most disruptive changes which must be immediately implemented: No more pass-through accounts for operational efficiency. No more sneaky or all-encompassing consent for data collection – consent must be explicit, specific, and withdrawable. No more willy-nilly accessing borrowers’ files, media, contact list, call logs or telephony functions. And no more discretionary reporting to credit bureaus – all loans including deferred payment products must be reported. Now the RBI is still mulling over first-loan-default-guarantees and hasn’t banned them yet.

? RBI gives PA hopefuls a second chance

It’s been a tough year for payment aggregators (PAs). The RBI has reportedly rejected the vast majority of PA applications. A common reason for rejection: failure to meet the net worth requirement of Rs.15 crores by 31 March 2021. Rejected PA applicants had to cease their activities within 6 months. But due to the large number of rejections, enforcing this requirement may cause major disruption. So, the RBI opened a second window for PA applicants. PAs which existed in March 2020 can now apply for authorization till 30 September 2022 if they have minimum net-worth of Rs.15 crores by 31 March 2022.

? Neo thoughts on neobanks

Niti Aayog proposed a licensing framework for full-scale neobanks (unlike the partnership based, front-end ones today) in a discussion paper last year. Now, after stakeholder consultations, it has released a revised proposal in a report. This report doesn’t deviate much from the original proposal. Except, it now suggests that two categories of licenses – one for business and retail consumers each – would be better. Because consumer facing neobanks focus on offerings like spend analytics and digital debit cards. While business facing ones focus on offerings like expense and payroll management. Many stakeholders had also specifically requested for this distinction. While we’re enthused, the RBI’s reportedly not a big fan of this proposal. And until the RBI changes its mind, this proposal must wait.

? SEC v. Crypto Insider Trading

Almost everyone involved in the crypto ecosystem has grappled with this question – are cryptos securities? The US Securities and Exchange Commission (SEC) is confident some of them are. Recently, the SEC filed insider trading charges against a former Coinbase product manager and two others. The SEC alleges that the accused passed on sensitive information about upcoming crypto listing announcements to his co-accused. And the co-accused profited using this information, buying the cryptos in question (before the listing announcement) and selling them shortly after. The SEC believes that 9 cryptos traded by the accused were securities. This could have a ripple effect across the ecosystem. For if these cryptos were securities, Coinbase could be acting as an unregistered broker or exchange. And the issuers of these cryptos could face action for issuing unregistered securities. What’s interesting though is that the US Justice Department, the other investigating agency, didn’t press any charges of securities fraud against the accused.

? Finding WazirX’s Wazir

No one in India truly knows who owns India’s largest crypto exchange – WazirX. Up until an Enforcement Directorate investigation last month, it was a matter of fact (or believed to be) that Binance owned WazirX. Even announcements from the two entities said so. After the investigation however, WazirX founder and the Binance CEO have each come up with their own version of events. And each denies owning WazirX. On its part, Binance has disabled off-chain transfers (transactions outside of blockchain) with WazirX, paralysing users’ ability to transfer funds between the two exchanges. And Binance’s CEO, CZ, has urged WazirX users to move their funds to Binance. This public ownership spat can only end badly for the third stakeholder – the users.

***************************************************************************************************

Main Course ?

⚠️ No more bonding the rules

Retail investor interest in the Indian equity markets is at an all-time high. During the pandemic, as Nifty and Sensex rallied to reach new peaks, retail investors poured money into everything from blue-chip to penny stocks. But another segment of the capital markets – corporate bonds – has also witnessed phenomenal growth during this period.

Historically, India’s corporate bond market has been relatively underdeveloped. A company can publicly issue bonds through stock exchanges or privately issue them through the Electronic Book Provider Platform. Around 98% bond issuances in India happen through private placement and to institutional investors. Till recently, retail investor participation in the primary and secondary bond market was negligible. However, with the advent of online bond trading platforms, the tide is turning. Since 2020, the number of users has increased 24 times and the value of retail trades has increased 6 times for these platforms. SEBI has been cautiously monitoring this trend and it’s decided to step in before the genie escapes the bottle.

SEBI’s latest consultation paper on regulation of online bond trading platforms proposes four key measures. First, these platforms must register as stockbrokers in the debt segment. Second, trading of bonds must be routed through stock exchanges. Third, bonds of unlisted companies must not be offered to the public. Fourth, a lock-in period of 6 months must be observed from the date of allotment in case of privately placed listed bonds. Because if these bonds are re-sold to more than 200 investors within a short period, it may amount to a deemed public issue.

Industry stakeholders have appreciated SEBI’s attempt to promote orderly growth of the bond market. However, some of the proposals have raised concerns. First, the prohibition on offering unlisted bonds and the 6-month lock-in period for privately placed listed bonds means that only a miniscule portion of bonds will be available to retail investors. Second, the prohibition on offering unlisted bonds may create another grey market for trading of ineligible bonds. A better alternative can be allowing unlisted bonds to be offered through regulated channels with adequate risk disclosures. Third, many bond trading platforms work with clearing corporations and depositories to enable trades. The money paid by investors is deposited in the clearing corporation’s bank account and the bonds are sent to the investors’ demat accounts. In this model where the platform doesn’t handle investor funds, the payment and settlement mechanism may not require tweaking. Fourth, current SEBI regulations prescribe a large lot size of Rs.10 lakh for privately placed bonds. But it’s unclear whether this requirement extends to unlisted bonds. And some platforms let retail investors purchase unlisted bonds in smaller lots. Unfortunately, the consultation paper doesn’t provide clarity about this issue.

Bonds offer a middle path for retail investors who want higher returns than fixed deposits but lower risk than stocks. As the world battles stagflation, they may be the goldilocks solution for investors looking to park their money. And SEBI will have to perform a fine balancing act to ensure both investor protection and a liquid bond market.

? Gamification of insurance

While taking an insurance policy in 1933, Dunn knew that her husband (who was going to use her car) was a dangerous driver. Yet, she hid this fact from her insurance company. A few years later, her husband crashed the car. The company dishonored the claim because Dunn hid an important fact – the driver’s behavior.

But is the driver’s behavior relevant? In India, it’s not. Car insurance premiums are usually based on the car’s features like engine capacity etc. But things are about to change. IRDAI has permitted general insurance companies to introduce three tech-enabled concepts for motor vehicles’ Own Damage cover. The most interesting one is ‘Pay How You Drive’ (PHYD) cover. Here, the driver’s behavior is considered while deciding the premium. For e.g., Mr. Ace Driveris charged less premium because he drives within speed limits. Whereas Mr. Risky Business is charged more because he often drives rashly, with quick accelerations and abrupt brakes.

But IRDAI’s move is preceded by two developments. One in the realm of law. The other in technology.

Development in Law:Earlier, IRDAI fixed insurance premiums (tariffs) that could be charged in India. But in 2007, it de-tariffed Own Damage cover. This allowed insurers to freely determine insurance premiums (except for Third-Party Damage covers). This flexibility is essential for insurers to deliver products like PHYD. If IRDAI had continued to fix tariffs, Mr. Ace Driver and Mr. Risky Business would’ve paid the same insurance premium. But because of this flexibility, Mr. Ace Driver pays a lot less.

Development in Technology: Cars have undergone a huge transformation – from purely mechanical to fully electric. As cars incorporated electrical components, it became easier to capture car movements. This is done using telematics devices.These devices are fitted into the vehicle. And they record speed patterns, acceleration and braking patterns, duration and location of the journey etc. This information is then relayed to the insurer and analyzed to determine driving behavior.

Products like PHYD policies are usually referred to as ‘Telematics Insurance’. These policies are heavily dependent on data. And various iterations of these products can be created – by using different data points to assess risk. For PHYD, these data points are speed, acceleration and braking patterns etc. Another product – ‘Pay As You Drive’ cover uses the total distance traveled (per month) to assess risk. The rationale is that if you drive less, your risk is lesser. Thus, data is a critical input for Telematics Insurance. And so, privacy risks must be balanced with benefits of such products.

A risk-based approach is needed while applying data privacy principles to telematics data. Because all telematics data may constitute ‘personal data’. But not all data points pose a similar risk of harm. For e.g., the driver’s braking pattern might pose lesser risk of harm than the car’s location data which may reveal visits to abortion clinics, political meetings, religious venues etc. And so, braking pattern data may not be regulated as onerously as location data. Insurers should also weigh the privacy risks of their data collection activities. And avoid collecting data points which pose a significant privacy risk, but don’t add real value in assessing the insurance risk. For e.g., a car’s location data may not necessarily add value in assessing the insurance risk.

Conclusion: Today, Mr. Ace Driveris paying a higher premium and subsidizing the insurance costs of Mr. Risky Business. But Telematic Insurance has enabled the gamification of insurance. Drivers are incentivized (through lower premiums) to drive safely and disincentivized (through higher premiums) to drive rashly. But this is limited to Own Damage covers. The IRDAI still notifies the tariffs for Third Party Damage covers. So, for gamification of insurance to have a real impact, Telematics Insurance pricing should be permitted for Third-Party Damage covers as well.

While IRDAI has its reasons to prescribe tariffs, IRDAI could consider prescribing tariff brackets based on risk scores. Here, the insurer could calculate the risk score using telematics data. And then decide the insurance premium based on IRDAI’s tariff brackets. Because like Lord Hanworth said (while deciding Dunn’s case) “… there is a greater risk in insuring a person who is likely to have an accident because of the way he drives a car”.

*************************************************************************************************

Dessert ?

? UPI scales new heights

In a move that’s sure to irk Mr.100, UPI set a new record by crossing 6 billion transactions in July. And in another 5 years, UPI hopes to process 1 billion transactions per day! Talk about being an overachiever. But how will UPI meet this goal? For starters, multiple payment systems are being linked with UPI. All e-wallets had to be made interoperable via UPI by 31 March 2022. And now, credit cards must also be linked with UPI, beginning with Rupay credit cards.

There are, however, a few hiccups. For instance, UPI transaction failure rates are high. About 1 in 10 UPI transactions face technical or business decline. The technical decline rates are especially high for public sector banks like SBI. NPCI is currently trying to implement a real-time fix for funds stuck due to failed transactions. But the problem is more fundamental. Due to the zero-merchant discount rate policy, banks have little incentive to upgrade their tech infrastructure to process UPI transactions. Which means higher technical decline rates. And if they must process 1 billion UPI transactions per day for free, we can only imagine how high their losses will be.

*************************************************************************************************

Takeaway ?

- A round-up of SEBI’s policy priorities and their potential impact on wealth-tech companies [Live Mint]

- An exploration of how capping interchange fees sparked fintech innovation in the US [Ramp]

- A deep dive into the history of failed crypto hedge fund, Three Arrows Capital, which took the market down with it [NY Mag]

- An explainer on why you can’t just ‘copy-paste’ WhatsApp’s code to Facebook Messenger to make it end-to-end encrypted [Verge]

- An analysis of an unusual year in finance [Economist]

*************************************************************************************************

That’s it from us. We’d love to hear from you. Tell us what you think about the stories we covered. You can write to us at contact@ikigailaw.com. See you in September.

If you enjoyed this edition, do share it with colleagues and friends.